LONDON (Realist English). On 14 May, the global oil market remained on edge. Brent crude prices hovered around $105–107 per barrel, while WTI traded near $102, reacting sharply to every statement coming from Beijing, where US President Donald Trump and Chinese President Xi Jinping are holding a summit.

The main driver of volatility remains the situation surrounding the Strait of Hormuz, through which roughly 20% of global oil and LNG consumption passed before the conflict erupted.

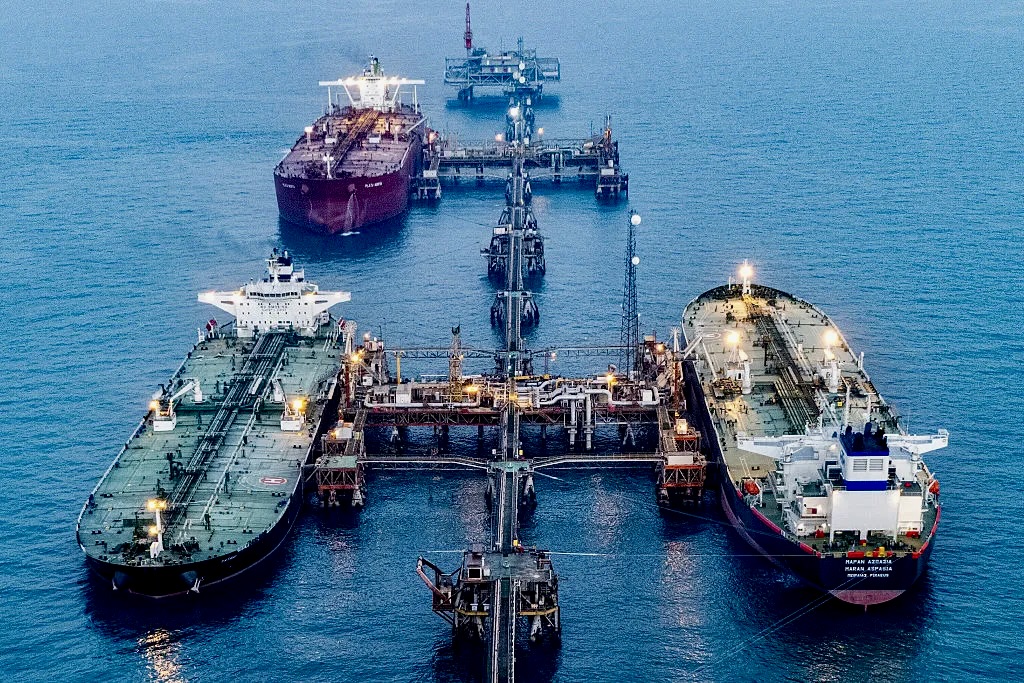

Price dynamics on 14 May

According to exchange trading data, by midday on 14 May the market looked as follows:

| Instrument | Price | Change | Comment |

| Brent (July futures) | $105.68/bbl | +0.1% | Asian trading |

| WTI (June futures) | $101.08/bbl | +0.1% | Asian trading |

| Brent (13 May close) | $107.95/bbl | +0.17% | after IEA forecast |

| WTI (13 May close) | $102.77/bbl | +0.58% | after US inventory report |

Macroeconomic backdrop: from deficit to fears of oversupply

The fundamental picture in the oil market remains deeply contradictory.

The International Energy Agency (IEA) has radically revised its outlook. While in April the agency expected a supply surplus, it now forecasts a deficit of 1.78 million barrels per day in 2026. Global demand is estimated at 104.03 million bpd, while supply stands at 102.2 million bpd.

In its report, the IEA stressed: “An acute supply deficit will persist through the end of the third quarter of 2026, even if the conflict ends by early June.”

Global commercial oil and petroleum product inventories have fallen from 8.6 billion barrels before the conflict to 8.1 billion barrels. The net deficit is estimated at 500–600 million barrels.

In March, the market recorded a record quarterly stock draw of 85 million barrels, while the second quarter is expected to see a deficit of 8.5 million barrels per day.

At the same time, OPEC lowered its forecast for global oil demand growth in 2026 for the first time since August — to 1.17 million bpd from the previous estimate of 1.38 million. However, its 2027 forecast was revised upward by 200,000 bpd to 1.54 million.

Strait of Hormuz remains the key risk factor

The Strait of Hormuz, blockaded by Iran since 28 February, remains the central driver of price instability.

The situation has changed little: commercial shipping through the strait has effectively halted. Before the war, up to 130 vessels per day transited Hormuz. Analysts now estimate that around 1,600 tankers remain stranded near the strait awaiting a resolution.

The key difference from April’s forecasts lies in the duration of the crisis. Most analysts initially expected the blockade to last one or two months, but it is now increasingly clear that it could continue at least through mid-May.

Some analysts, including Fitch Ratings, are modelling scenarios in which the strait remains closed for as long as five months.

US shale industry cannot offset the deficit

Prices above $100 per barrel were expected to trigger a sharp increase in US shale production. So far, that has not happened.

According to Jefferies, even with WTI prices around $85 per barrel, additional shale output growth would amount to only about 55,000 bpd — far too little to cover the current deficit.

At current price levels, growth in the US shale sector remains limited.

The gas market is showing similar dynamics. LNG cargoes transiting via Hormuz have become significantly more expensive, while the spread between the US Henry Hub benchmark and international gas markets has widened to multi-year highs.

Forecasts from Western analysts

Analysts remain divided into two camps: those who see current prices as sustainable, and those expecting a sharp market reversal.

| Analyst / Organization | Brent Forecast | Key Thesis |

| TD Securities (Ryan McKay) | 150 $ | “The calm is temporary. Storms are approaching.” |

| S&P Global Ratings | Around $100 through end-2026 | Forecast raised by $15 due to prolonged blockade |

| US EIA | Q2 peak: $106–115 | Then decline to $79 by 2027 |

| Goldman Sachs | $90 in Q4 2026 | Forecast lowered, but escalation risks remain |

| Fitch Ratings | $100–110 in May–July | Then possible fall to $70 by September |

| UBS (Giovanni Staunovo) | Depends on negotiations | “The market reacts to every headline.” |

| The Economist | Around $88 by year-end | Futures markets expect cooling prices |

Conclusions and outlook

The global oil market has reached a crossroads.

On one side, hard fundamentals — record inventory deficits, the ongoing Hormuz blockade, and revised forecasts from the IEA and OPEC — continue pushing prices higher.

On the other, hopes for a diplomatic settlement and warnings of a future supply surplus from the US Energy Information Administration (EIA), Fitch and Goldman Sachs are capping bullish momentum.

TD Securities warns: “The calm in the market is temporary. Storms are approaching that could push Brent to $150 and above.”

Meanwhile, the US EIA forecasts that prices could fall to $79 by 2027 as Middle Eastern production gradually recovers.

Ultimately, the future trajectory of the oil market will depend primarily on the political outcome of negotiations: whether a deal with Iran can be reached and whether the Strait of Hormuz will reopen.

If diplomacy fails, the scenario of $150 oil could materialise far faster than many optimists currently expect.